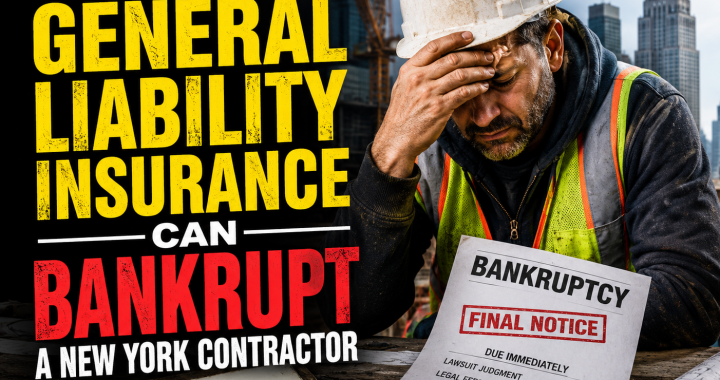

Most New York contractors believe that once they purchase a commercial general liability (CGL) policy, they are protected against lawsuits and property damage claims. Unfortunately, that assumption can prove devastatingly wrong.

In today’s insurance marketplace, especially in New York construction, many policies contain exclusions and limitations that can significantly reduce or even eliminate coverage for some of the most common construction-related claims. Contractors often discover these hidden exclusions only after a claim occurs—when it is too late to purchase additional protection.

With New York’s aggressive litigation environment, complex Labor Law exposures, and increasingly restrictive underwriting standards, understanding what your general liability policy does not cover may be just as important as understanding what it does cover.

Here are some of the most important hidden general liability exclusions that every New York contractor should know about.

1. Action-Over Exclusions

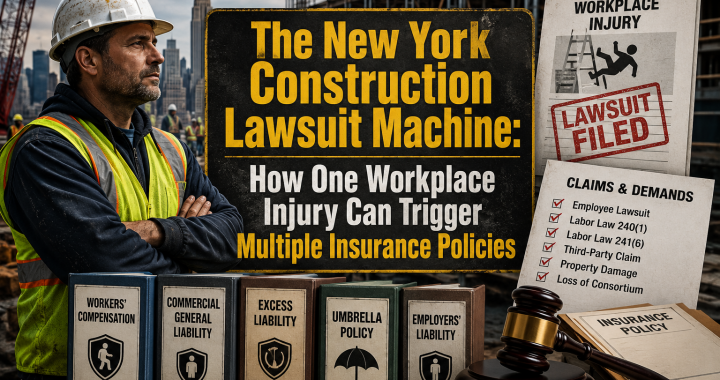

Perhaps no exclusion creates more concern for New York contractors than the action-over exclusion.

New York Labor Law Sections 240 and 241 allow injured employees of subcontractors to pursue claims against general contractors and property owners under certain circumstances. An action-over exclusion can eliminate coverage for these claims, leaving contractors exposed to potentially catastrophic lawsuits.

Many contractors don’t realize their policy contains this exclusion until they receive a denial letter after a serious workplace injury.

If you perform construction work in New York, understanding your policy’s action-over language is critical.

2. Height Limitation Exclusions

Many general liability policies issued to contractors now contain strict height restrictions.

Examples include exclusions for work performed:

- Above two stories

- Above three stories

- Above fifteen feet

- Above thirty feet

This presents a serious problem because many contractors regularly perform work that exceeds these limits without realizing they may be operating outside their coverage parameters.

Roofers, painters, masons, restoration contractors, window installers, and siding contractors are particularly vulnerable to height restriction exclusions.

3. Residential Construction Exclusions

Numerous insurance carriers restrict or exclude work performed on residential projects.

A contractor may believe they have coverage for all operations only to discover their policy excludes:

- Single-family residences

- Multi-family housing

- Condominium projects

- Apartment buildings

- Mixed-use residential properties

Given the large amount of residential construction activity in New York, failing to identify these exclusions can create substantial uninsured exposure.

4. Subcontractor Warranty Endorsements

Many policies contain subcontractor warranty provisions that require contractors to obtain specific documentation before coverage applies.

These requirements often include:

- Written contracts

- Hold harmless agreements

- Additional insured endorsements

- Certificates of insurance

- Primary and non-contributory wording

- Waivers of subrogation

Failure to obtain even one required document may allow an insurer to deny coverage for a claim involving a subcontractor.

Many contractors mistakenly believe that simply receiving a certificate of insurance satisfies all policy requirements.

5. Exterior Insulation and Finish System (EIFS) Exclusions

EIFS claims have historically produced significant losses for insurance companies. As a result, many contractors’ policies specifically exclude work involving EIFS materials.

Contractors performing stucco, synthetic stucco, waterproofing, or exterior finishing operations should carefully review their policies to determine whether these exclusions apply.

Even contractors performing repair work on EIFS systems may discover they have little or no coverage.

6. Classification Limitation Endorsements

Insurance companies frequently issue policies restricting coverage only to the classifications specifically listed on the declarations page.

For example, a contractor insured as a carpenter who performs roofing, demolition, excavation, or concrete work may discover that these operations are excluded because they were never properly reported.

As businesses evolve and expand, coverage gaps can develop if operations are not updated regularly.

7. Designated Ongoing Operations Exclusions

Some policies specifically exclude certain operations, equipment, or activities.

Examples include exclusions for:

- Demolition

- Excavation

- Structural work

- Roofing

- Waterproofing

- Environmental work

- Lead or asbestos exposures

- Fire suppression systems

Contractors should review these endorsements carefully to ensure their actual operations match what the policy covers.

8. Professional Liability Exclusions

General liability insurance typically does not cover professional services.

Contractors who provide:

- Design services

- Engineering recommendations

- Construction management

- Project consulting

- Building specifications

may require separate professional liability coverage.

A contractor can be sued for professional negligence even if no physical property damage occurs.

9. Employee Injury Exclusions

General liability policies generally exclude bodily injury claims brought by employees.

Contractors sometimes mistakenly assume that if workers compensation denies a claim, their general liability policy will respond. In most cases, employee injury exclusions prevent this.

This makes maintaining proper workers compensation coverage absolutely essential.

10. Contractual Liability Limitations

Many construction projects require contractors to sign broad indemnification agreements.

However, not all contractual obligations assumed by contractors are covered under general liability policies.

Some contractual promises may extend beyond what the insurance policy actually covers, potentially creating significant uninsured liabilities.

Contractors should always have construction contracts reviewed carefully before signing.

Why These Exclusions Matter More in New York

New York remains one of the most challenging insurance environments in the country for contractors. High litigation costs, Labor Law exposures, rising jury verdicts, and increasingly restrictive insurance markets have forced many carriers to limit coverage through exclusions and endorsements.

A policy with a low premium may ultimately become the most expensive insurance purchase a contractor ever makes if a claim occurs and coverage is denied.

The difference between a properly structured policy and an improperly structured policy can literally determine whether a contractor survives a major lawsuit.

Three Common Google Searches Contractors Use When Looking for General Liability Help

Contractors searching for answers regarding coverage problems frequently use search phrases such as:

- “Best general liability insurance for New York contractors”

- “What does contractor general liability insurance cover?”

- “Insurance broker specializing in New York construction insurance”

If you’re searching these phrases, it’s probably time to have your coverage reviewed by a professional who understands New York construction risks.

How BGES Group Can Help

BGES Group is a boutique insurance brokerage specializing in New York construction insurance. For more than 45 years, we have helped contractors navigate the increasingly complex insurance marketplace while identifying potential coverage gaps before they become financial disasters.

We specialize in:

- Commercial General Liability Insurance

- Workers Compensation Insurance

- Umbrella and Excess Liability Coverage

- Builders Risk Insurance

- Contractor Package Policies

- Commercial Auto Insurance

- Surety and Bonding Programs

- Subcontractor Risk Management

- Contract Review Assistance

- Construction Risk Analysis

Unlike many large insurance agencies where accounts may be serviced by multiple people, BGES Group provides personalized service with direct access to experienced construction insurance professionals who understand the unique challenges facing New York contractors.

Our goal is simple: help contractors identify coverage gaps, reduce risk, and protect the businesses they have worked so hard to build.

Contact BGES Group

Gary Wallach

BGES Group

Phone: (914) 806-5853

Email: bgesgroup@gmail.com

Website: BGES Group

Informational Disclaimer: This article is provided for educational and informational purposes only and does not constitute legal, insurance, tax, or professional advice. Insurance policies vary significantly by carrier, endorsement, and jurisdiction. Coverage determinations depend upon the specific terms, conditions, exclusions, and endorsements contained within each individual policy. Contractors should consult qualified legal counsel and licensed insurance professionals regarding their particular circumstances and insurance needs before making coverage decisions.