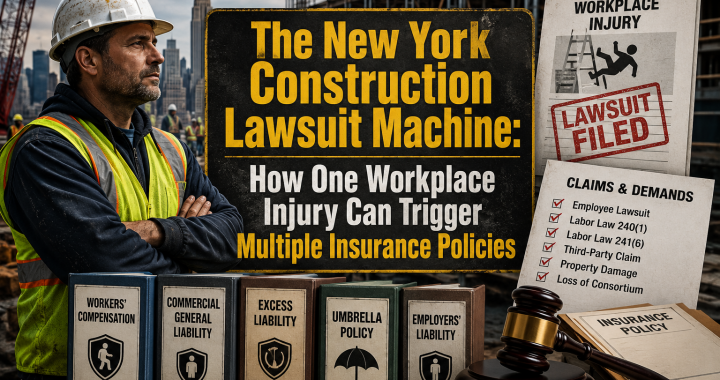

For contractors operating in New York, every construction project carries risk. Most contractors understand the obvious dangers: falls, equipment accidents, property damage, and workplace injuries. What many contractors, property owners, and even some insurance professionals fail to appreciate is how a single workplace accident can trigger a cascade of lawsuits, insurance claims, and legal obligations involving numerous parties and multiple insurance policies.

In New York’s unique legal environment, one construction injury can quickly evolve into a complex web of litigation involving workers compensation carriers, general liability insurers, umbrella carriers, property owners, general contractors, subcontractors, and excess insurance companies. Understanding how this process works is critical for protecting your business, your assets, and your future.

One Accident. Multiple Lawsuits.

Imagine the following scenario.

A masonry subcontractor’s employee is working on scaffolding at a commercial construction project in New York. While performing routine work, the scaffold shifts, causing the worker to fall two stories and suffer severe injuries.

What happens next?

Most contractors assume the employee files a workers compensation claim and the matter ends there.

In New York, that’s often only the beginning.

The injured worker immediately files a workers compensation claim through his employer’s workers compensation insurance carrier. Medical bills begin accumulating. Wage replacement benefits commence.

Then the injured worker’s attorney files lawsuits against:

- The property owner

- The general contractor

- The construction manager

- Other contractors on the project

- Equipment manufacturers, if applicable

What initially appeared to be a workers compensation claim has now become a major liability lawsuit.

Why New York Labor Laws Change Everything

New York Labor Law Sections 240 and 241 create some of the most challenging liability exposures in the country.

Labor Law 240, often called the “Scaffold Law,” imposes extraordinary liability on owners and contractors for gravity-related accidents, including falls from heights and injuries caused by falling objects.

Labor Law 241 imposes additional obligations related to construction site safety and compliance with New York Industrial Code regulations.

As a result, injured workers frequently sue virtually every entity associated with a construction project.

The damages sought often include:

- Medical expenses

- Lost wages

- Future lost earnings

- Pain and suffering

- Permanent disability

- Loss of quality of life

- Future medical care costs

These claims can easily reach millions of dollars.

Workers Compensation: The First Layer

The first insurance policy typically triggered is workers compensation insurance.

Workers compensation provides:

- Medical treatment

- Wage replacement

- Rehabilitation expenses

- Disability benefits

- Death benefits, if applicable

Many contractors mistakenly believe that workers compensation is the exclusive remedy.

While workers generally cannot sue their direct employer, they often retain the right to sue numerous third parties involved in the construction project.

This distinction is what creates the “construction lawsuit machine” that New York contractors face every day.

The General Liability Policy Gets Pulled In

Once the injured worker files suit against the owner and general contractor, those defendants frequently seek defense and indemnification from the employer-subcontractor.

This process triggers the subcontractor’s commercial general liability policy.

The general liability carrier now faces potential exposure for:

- Legal defense costs

- Settlement negotiations

- Trial expenses

- Indemnification obligations

- Additional insured obligations

The costs associated with defending a serious construction accident can reach hundreds of thousands of dollars before a case ever reaches trial.

Additional Insured Coverage Becomes Critical

Most construction contracts require subcontractors to provide additional insured status to upstream parties.

As a result, the subcontractor’s insurance company may also become responsible for defending:

- Property owners

- General contractors

- Construction managers

- Developers

One accident can therefore require a single insurance company to provide legal representation and coverage to multiple defendants simultaneously.

This is why additional insured endorsements are among the most important risk transfer tools in the construction industry.

Without proper additional insured coverage, contractual disputes and uninsured exposures can quickly emerge.

The Action-Over Claim

One of the most feared scenarios in New York construction is the action-over claim.

Here’s how it develops:

- The employee receives workers compensation benefits.

- The employee sues the owner and general contractor.

- The owner and general contractor file claims against the employer-subcontractor.

- The subcontractor’s liability insurance becomes involved.

What started as a workers compensation claim has transformed into a complex liability lawsuit involving multiple parties and multiple insurance carriers.

For contractors with inadequate insurance coverage, action-over claims can be financially devastating.

Umbrella and Excess Liability Coverage

Serious construction accidents rarely remain within the limits of primary insurance policies.

Consider the following example:

- General liability limit: $1 million

- Settlement demand: $7 million

Where does the additional $6 million come from?

This is where umbrella and excess liability policies become essential.

Excess liability coverage provides additional layers of protection once primary limits have been exhausted.

In New York construction, catastrophic injury claims involving paralysis, traumatic brain injuries, amputations, or wrongful death can result in settlements and verdicts exceeding $10 million, $20 million, or even higher.

Contractors who fail to purchase adequate umbrella coverage often discover the true value of insurance only after disaster strikes.

Contractual Indemnification

Construction contracts typically contain indemnification provisions requiring one party to protect another from liability.

These provisions often trigger additional disputes involving:

- Contract interpretation

- Insurance obligations

- Defense responsibilities

- Risk transfer provisions

- Additional insured status

Multiple law firms, insurance adjusters, and experts may spend years litigating who ultimately bears responsibility for a single accident.

The legal expenses alone can be enormous.

The Hidden Cost of Cheap Insurance

Many contractors purchase insurance based primarily on price.

Unfortunately, low-cost policies often contain restrictions such as:

- Labor Law exclusions

- Height limitations

- Action-over exclusions

- Employee injury exclusions

- Residential construction exclusions

- Restrictive additional insured endorsements

The contractor believes they have purchased protection.

The insurance company believes it has limited its exposure.

The disagreement often becomes apparent only after a major claim occurs.

By then, the contractor may face millions of dollars in uninsured liability.

Protecting Your Construction Business

The best defense against New York’s construction lawsuit environment involves several critical components:

- Strong workplace safety practices

- Proper subcontractor agreements

- Comprehensive insurance coverage

- Adequate umbrella liability limits

- Effective contractual risk transfer

- Proper additional insured endorsements

- Experienced legal and insurance advisors

Insurance should never be viewed simply as an expense.

It is a financial protection system designed to preserve the business you have spent years building.

Experience Matters

New York construction insurance is among the most specialized and complex areas of commercial insurance.

A contractor’s insurance program should not simply satisfy a contract requirement.

It should be designed to survive the realities of New York construction litigation.

The difference between surviving a catastrophic claim and losing everything often comes down to the experience and expertise of the professionals designing your insurance program.

About BGES Group

At BGES Group, we specialize in helping contractors navigate the challenging world of New York construction insurance.

For more than 45 years, owner Gary Wallach has worked with contractors throughout New York, New Jersey, and Connecticut, helping businesses secure comprehensive protection while controlling insurance costs and managing risk.

Our areas of expertise include:

- General Liability Insurance

- Workers Compensation Insurance

- Excess and Umbrella Liability

- New York Labor Law Exposures

- Additional Insured Requirements

- Contractual Risk Transfer

- Contractor Package Policies

- Commercial Auto Insurance

- Builder’s Risk Insurance

- Contract Review Assistance

- Specialized New York Contractor Insurance Programs

As a boutique agency, BGES Group provides personalized service that many larger agencies cannot match. We understand New York construction risks, issue certificates quickly, respond rapidly to client needs, and work directly with contractors to identify potential gaps in coverage before losses occur.

If you are a contractor, subcontractor, property owner, or developer operating in New York, we welcome the opportunity to review your current insurance program and help ensure your business is properly protected.

Gary Wallach

BGES Group

Phone: 914-806-5853

Email: bgesgroup@gmail.com

Website: www.bgesgroup.com

Important Financial and Informational Disclaimer

This article is provided solely for informational and educational purposes and does not constitute legal, insurance, financial, tax, or risk management advice. Insurance coverages, policy forms, endorsements, contractual obligations, and legal liabilities vary substantially depending upon the facts and circumstances involved. Readers should consult qualified legal counsel and licensed insurance professionals regarding their specific situations. Coverage availability, policy provisions, underwriting requirements, and pricing vary among insurance carriers. No representation, warranty, or guarantee of coverage, legal outcome, or future results is expressed or implied.