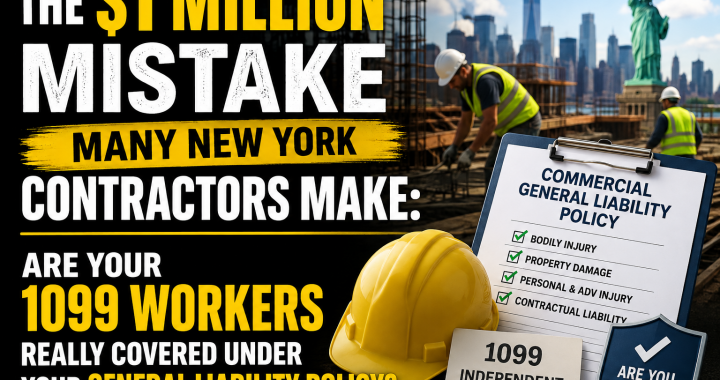

One of the biggest misconceptions in the construction industry is that tax classification determines insurance coverage. In reality, your Commercial General Liability (CGL) insurance policy may view these workers very differently than the IRS or your accountant does.

Understanding how your insurance company classifies 1099 workers—and how your policy’s subcontractor warranty or “Hard Hammer” endorsement applies—could mean the difference between having a claim paid or having coverage denied.

Does a 1099 Automatically Make Someone an Independent Contractor?

The answer is no.

A Form 1099 is simply a tax reporting document. It does not determine whether someone is considered an employee or an independent contractor under your Commercial General Liability policy.

When evaluating a claim, insurance companies often look at the actual working relationship between the contractor and the worker. Factors may include:

- Who controls how the work is performed.

- Who supplies the tools and equipment.

- Whether the worker performs services exclusively for one contractor.

- Whether the worker has their own business.

- Whether the worker carries their own insurance.

- Whether the worker hires and supervises their own employees.

Depending on these facts, a carrier may determine that a 1099 worker is actually functioning as your employee or, alternatively, as an uninsured subcontractor.

Why This Matters

Many contractors purchase insurance without fully understanding the endorsements attached to their policy.

One endorsement that has become increasingly common in the New York construction market is the Hard Hammer Subcontractor Warranty.

While the wording varies among insurance companies, these endorsements generally require that every subcontractor satisfy specific insurance requirements before beginning work.

If those requirements are not met, the insurance company may significantly reduce or completely eliminate coverage for claims arising out of that subcontractor’s work.

What Is a Hard Hammer Subcontractor Warranty?

A Hard Hammer endorsement is designed to transfer risk from the insurance company back to the insured contractor.

To comply with many of these endorsements, contractors are typically required to obtain documentation from every subcontractor before work begins.

Common requirements include:

- A signed written subcontract or hold harmless agreement executed before work starts.

- Proof that your company has been added as an Additional Insured.

- Additional Insured status provided on a Primary and Non-Contributory basis.

- A Waiver of Subrogation in your favor.

- Commercial General Liability limits of at least $1,000,000 per occurrence (or higher if required).

- Active Workers’ Compensation insurance.

- Certificates of Insurance verifying the required coverages.

If even one of these requirements is missing, your policy’s Hard Hammer endorsement may be triggered.

What Happens if Your 1099 Worker Is Considered an Independent Contractor?

This is where many contractors encounter serious problems.

Suppose you hire a 1099 worker to perform framing work on one of your projects.

You never execute a written subcontract.

You never obtain a certificate of insurance.

You never require Additional Insured status.

There is no Primary and Non-Contributory wording.

No Waiver of Subrogation is obtained.

The worker has no Workers’ Compensation policy.

Several months later, property damage or bodily injury occurs arising out of that worker’s operations.

If your insurance carrier determines that the individual was actually an independent contractor rather than your employee, they may conclude that your Hard Hammer endorsement has not been satisfied.

Depending upon the wording of your policy, this could result in:

- Reduced coverage.

- Higher deductibles or self-insured retention.

- Limited defense obligations.

- Denial of indemnity.

- Complete denial of coverage for the claim.

Every policy is different, and coverage depends on the specific policy language, endorsements, facts of the claim, and applicable law. However, contractors should never assume that using a 1099 worker automatically satisfies their insurance requirements.

The Hidden Risk

Many contractors spend thousands of dollars purchasing liability insurance but unknowingly create coverage gaps by failing to properly document their subcontractors.

During audits or after a serious claim, insurance companies frequently request:

- Written contracts.

- Certificates of Insurance.

- Additional Insured endorsements.

- Hold Harmless Agreements.

- Workers’ Compensation documentation.

If these records cannot be produced, questions may arise regarding whether the subcontractor warranty has been satisfied.

Waiting until after a claim occurs is far too late.

Best Practices for New York Contractors

Whether you hire one subcontractor or one hundred, every contractor should establish procedures before anyone begins work.

Consider implementing the following practices:

- Require written contracts before work starts.

- Obtain certificates of insurance before workers arrive on the job.

- Verify that Additional Insured endorsements have actually been issued—not merely promised.

- Confirm Primary and Non-Contributory wording.

- Obtain Waivers of Subrogation where required.

- Verify active Workers’ Compensation coverage.

- Review liability limits to ensure they meet your contractual requirements.

- Keep organized electronic records for every subcontractor.

These simple administrative steps can help protect your company if a claim arises.

Don’t Assume—Know What Your Policy Requires

Every Commercial General Liability policy is different.

Some policies contain soft subcontractor warranties while others contain much stricter Hard Hammer endorsements. The exact wording of the endorsement can dramatically affect how coverage is applied following a claim.

Because of this, contractors should have their policies reviewed by an insurance professional who understands New York construction risks and can identify potentially dangerous endorsements before a loss occurs.

Spending a few minutes reviewing your policy today may save your business hundreds of thousands—or even millions—of dollars in uncovered claims tomorrow.

About BGES Group

At BGES Group, we specialize in insurance solutions for New York contractors. With more than 45 years of insurance experience, we understand the unique risks facing the construction industry, including subcontractor compliance, Commercial General Liability, Workers’ Compensation, Builders Risk, Umbrella Liability, Commercial Auto, and contractor-specific insurance requirements.

Our goal is not simply to sell an insurance policy—we help contractors understand what their policies actually cover and identify potentially dangerous exclusions and endorsements before they become expensive problems.

If you’re unsure whether your current policy contains a Hard Hammer subcontractor endorsement, or you’d like a second opinion on your insurance program, we’d be happy to review it with you.

Gary WallachBGES Group

Phone: 914-806-5853

Email: bgesgroup@gmail.com

Website: www.bgesgroup.com

Disclaimer: This article is for general informational purposes only and is not legal or insurance coverage advice. Insurance coverage depends on the specific policy language, endorsements, facts of each claim, and applicable law. Contractors should consult with their insurance professional and legal counsel regarding their specific circumstances.