Once they have paid their annual premium, many employers pay scant attention to their workers’ comp policy until the renewal date starts closing in. Unfortunately, that’s not the best time to attempt to control costs.

Because workers’ comp is one of the most loss-sensitive insurance policies, and as claims can sometimes be paid out for decades, it’s important that you proactively manage claims. One way to do that is through a quarterly claims review process, the timing of which is in line with the calculation of your company’s Experience Modification Factor (X-Mod).

It’s important to review loss runs and assess all open claims three months into the new policy year, because the critical number crunching for calculating the X-Mod takes place six months after the policy anniversary date. This gives you three months to reduce or close claims that will affect the X-Mod calculation.

Policies that renewed on Jan. 1, 2020 used the loss experience from policies that were effective from 1/1/16 to 2/31/16; from 1/1/17 to 12/31/17; and from 1/1/18 to 12/31/18. In other words, it looks at the claims from four years ago to one year prior. It will not include the most recent year’s claims payouts, as they are still too fresh.

This is when it’s time to focus on trying to close claims and reducing reserves on existing claims. The top priority is getting the injured employees back to full or modified duty. If that isn’t possible and return to work appears unlikely, then consideration should be given to settling the claim.

Six months after policy inception is the most important day of the workers’ comp year, because this is when the insurance company sends loss information to your state’s rating bureau to be used in the calculation of your X-Mod. This is known as the valuation date, or sometimes, the unit stat date.

This information includes not only the money that the insurer has spent on claims, but also what it expects to spend (the reserves). In effect, your insurer takes a snapshot of your loss information and it is absolutely critical that these numbers are correct. With few exceptions, once the rating bureau has the numbers, they are set in stone.

Unfortunately, the numbers are often inaccurate because gauging claims costs is not an exact science. Also, errors are rampant in the system and, once an insurer sets reserves for a claim, it is hard to get them reduced until after the claim closes.

The window of opportunity is short and the process of correcting mistakes can take time, which is another reason for the comprehensive review three months after the policy’s inception.

Put reserves in focus

Pay close attention to reserves. They represent what the insurance company thinks the ultimate cost of the claim will be. It is not a guess, but it is more of an art than a science.

Its accuracy depends on the precision of the adjuster in evaluating the employee’s medical condition, anticipated time away from work, cost of medical care and other relevant costs.

Yet, the cost projections get counted exactly the same as the dollars paid out, so if the reserve is set too high, you will pay too much.

Although the X-Mod is set at the sixth-month mark, it is a good idea to continue the quarterly review process at nine months. Throughout the year, proactive management of all open claims will ensure that there are no surprises at renewal.

BGES Group’s office, located in Larchmont, NY is a full service insurance agency offering, Property, Liability, Umbrella Liability, Business Auto, Bid & Performance Bonds, Inland Marine, Worker’s Compensation, New York State Disability, Group Health, Life insurance, Personal lines and Identity Theft.

BGES Group’s office, located in Larchmont, NY is a full service insurance agency offering, Property, Liability, Umbrella Liability, Business Auto, Bid & Performance Bonds, Inland Marine, Worker’s Compensation, New York State Disability, Group Health, Life insurance, Personal lines and Identity Theft.

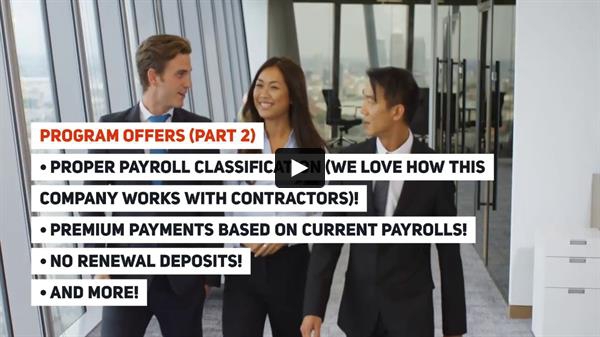

BGES Group are Worker’s Compensation Specialists for the States of New York, New Jersey and Connecticut – Issues we address: 1) Lowering pricing – we have specialty programs that can save you up to 40%; 2) Finding a new company; 3) Being cancelled or non renewed; 4) Audit disputes; 5) Company creating fictitious payroll at audit time; 6) Lowering high experience modifications factors; 7) Misclassification of payrolls; 8) Lowering or eliminating renewal deposits; 9) Getting coverage when you’ve been without for a few months; 10) Covering multiple states under one policy; 11) Eliminating 10% service or policy fees; 12) Timely issuance of certificates; 13) Always being able to get someone on the phone or by email when you need to.

Special Contractor Insurance Programs (NY, NJ, CT) – We we have 50+ insurance companies to market your general liability, umbrella liability, business auto, workers compensation, bid & performance bonds and group health coverages. We help contractors set up proper risk transfer mechanisms. If you’re a contractor we offer extensive information about insurance markets, coverages, risk transfer mechanisms, subcontractor screening, ways to lower your insurance costs that lower them.

Contractors Make More Sales – Close more sales with easy, affordable financing options for your customers. Everything can be done from your phone. Thirteen banks to get financing from. No hidden fees. Click here to learn more.

Identity Theft – Over the past year hundreds of thousands of people have had to deal with identity theft. This has become such a huge problem so we now offer Identity Theft Protection. We heard stories of kids going for car loans and learning they owe $200,000+ to companies they never heard of. Under our program you can protect yourself, spouse and children. Anyone you know can purchase this protection though our plan! Click here to learn more or sign up.

Soon To Be The Best Artificial Intelligence Technology Marketing Platform In The World To Get You New Customers – Sick and tired of paying social media experts thousands of dollars to do your marketing? Paying Google, Facebook, Linkedin hundreds/thousands of dollars for lousy results? How would you like to dominate your business niche? How would you like get in on the ground floor and earn a massive new cash flow every month? Click here to learn more.

If you would like to speak with us call Gary Wallach at 914-806-5853 or click here to email or click here to visit our website.

Company: BGES Group, 216A Larchmont Acres West, Larchmont, NY 10538

e-mail: bgesgroup@gmail.com

website: http://www.bgesgroup.com

© – Copyright – 2020 – BGES Group