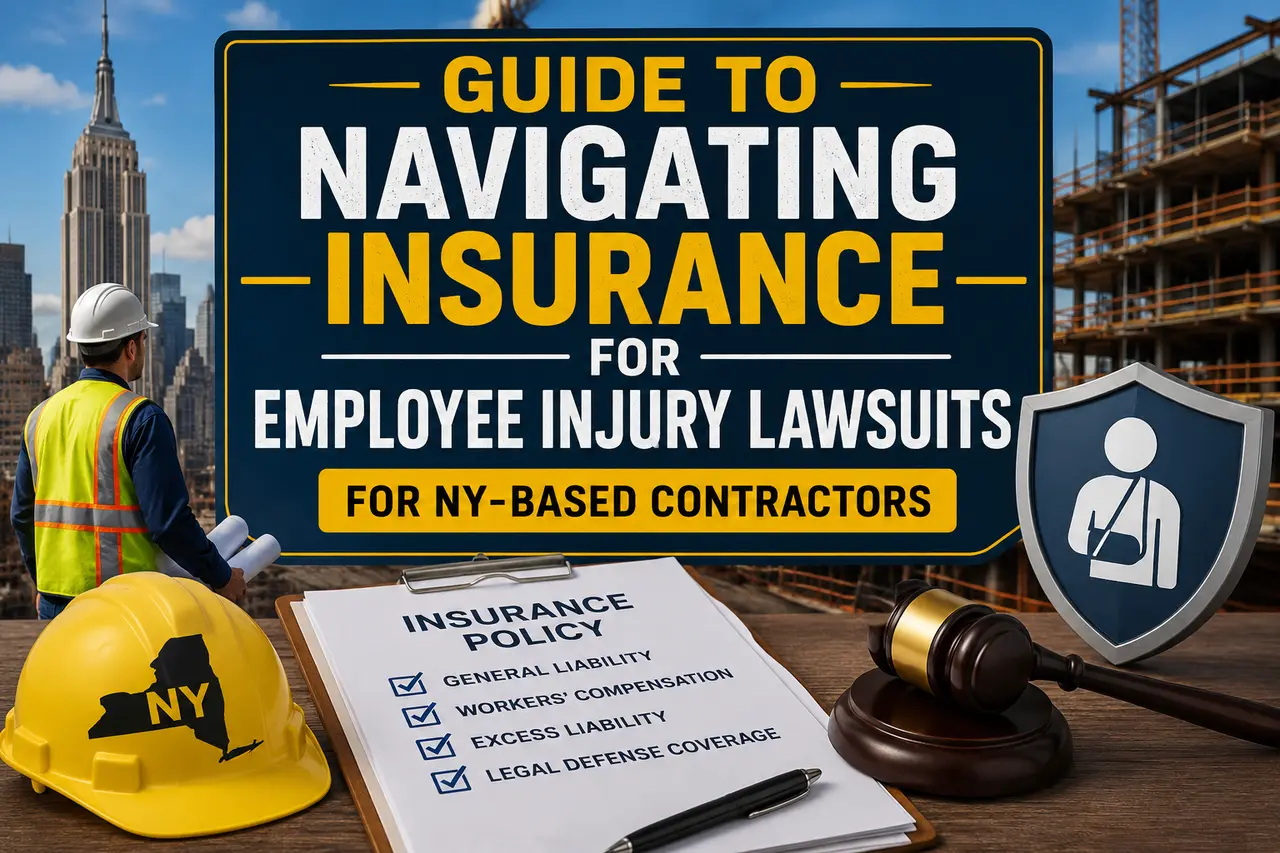

Navigating the maze of insurance for employee injury lawsuits can be daunting, especially for contractors based in New York. Understanding what insurance policies cover, how they protect your business, and the legal obligations involved is crucial. In this guide, we’ll break down everything you need to know in a simple, easy-to-understand way.

Understanding the Basics of Employee Injury Lawsuits

Employee injury lawsuits can stem from various incidents, including workplace accidents or alleged negligence. As a contractor in New York, it’s crucial to be aware that these lawsuits often arise when employees claim unsafe working conditions led to their injuries. Establishing a comprehensive safety protocol is an effective first step towards minimizing risks, but sometimes, no matter how safe you make the work environment, accidents can still occur. Knowing this, contractors should familiarize themselves with the typical legal proceedings in such cases. Most lawsuits will require clear documentation and evidence to either support or dispute claims. By having solid knowledge about how these lawsuits typically unfold, contractors can better prepare to defend their business interests.

Employee injury lawsuits are not only about workplace safety. Often, they involve a multitude of other factors such as compliance with labor laws and the adequacy of safety equipment provided to employees. Contractors must ensure that they’re not only providing these essentials but also maintaining satisfactory records of compliance. Documentation is essential in protecting your business in court. Maintaining detailed records and evidence of constant safety checks and training sessions can serve as valuable proof of due diligence, which is crucial when attempting to counteract any claims of negligence.

Types of Insurance Policies Relevant to Contractors

The primary types of insurance that contractors in New York might consider include workers’ compensation, general liability, and employer’s liability insurance. Workers’ compensation insurance is designed to cover medical expenses and a portion of lost wages for employees who suffer an injury while on the job. This insurance is not just a safeguard for employees; it also provides employers with a financial cushion against lawsuits arising from workplace injuries. Without such coverage, businesses may risk severe financial repercussions due to medical expenses and potential compensatory and legal payouts.

Employer’s liability insurance is another critical consideration. It typically covers the legal costs involved in defending against claims alleging employer negligence. Even if you meticulously follow all safety protocols, unfortunate incidents can happen, and employees may still file lawsuits. This is where employer’s liability insurance becomes invaluable. On the other hand, general liability insurance is broader; it protects against third-party claims of injury or property damage. Ensuring you have these policies can provide a peace of mind and support risk management strategies in your contracting business effectively.

The Importance of Workers’ Compensation in New York

In New York, workers’ compensation is not only crucial—it’s mandatory for most businesses. It is designed to ensure that employees who suffer work-related injuries get the necessary medical care and are financially supported during recovery. For contractors, this means having an active policy that complies with state regulations. Failure to provide workers’ compensation insurance can result in severe penalties, including fines and potential shutdowns.

It’s essential to understand that workers’ compensation serves as a no-fault insurance. This means that regardless of who is at fault for the injury, the employee is eligible for compensation. This stipulation underscores the importance of maintaining this type of insurance, as it protects both the employee and employer from lengthy litigation processes. By streamlining the process of providing care to injured workers, the insurance helps reduce the risk of lawsuit escalation, which is beneficial for maintaining business operations with minimal legal interruptions.

Evaluating Additional Coverage Options

Beyond the standard policies, contractors may also consider additional coverage options such as umbrella insurance. Umbrella policies provide a layer of security by covering amounts exceeding the limits of your other policies. For example, if a lawsuit results in damages that surpass the coverage of a general liability policy, an umbrella insurance policy can cover the difference. This type of coverage is particularly advantageous for NY-based contractors facing potential high-value claims. Accessing comprehensive coverage means safeguarding your business assets and ensuring sustainability even in challenging situations.

Another option is builders risk insurance, which provides coverage for buildings under construction. This can be invaluable in cases where employee injuries occur on sites yet to be fully developed or operational. By evaluating these and other specialized policies, you can find solutions tailored to the unique risks facing your specific operations. Investing in additional coverage options signifies not just compliance but strategic foresight in protecting long-term business interests.

Tips for Selecting the Right Insurance Provider

Selecting the right insurance provider can significantly impact the level of support your business receives during a lawsuit. When evaluating potential providers, reliability, and reputation are key factors. Consider seeking recommendations from industry peers or consulting business reviews to gauge satisfaction levels regarding claims handling and customer service. Transparency in policy terms and the willingness to customize solutions to meet your specific needs is also crucial. Look for insurers who showcase a proven track record of speedy claim resolution and robust support services.

Rates and premiums are important, but they shouldn’t be the sole criteria. Sometimes, a less expensive policy may result in higher out-of-pocket expenses during a claim. Ensure the coverage level offered meets your business’s risk tolerance and operational needs. Additionally, inquire about the availability of bundled packages, which may offer comprehensive coverage at a reduced rate. By taking a balanced approach, focusing on both cost and coverage quality, you’ll maximize your investment in insurance and ensure your business’s readiness for unforeseen events.

Steps to Take When Faced with an Employee Injury Lawsuit

When faced with an employee injury lawsuit, prompt action is essential. The first immediate step is to notify your insurance provider to initiate the claim process. Providing detailed information about the incident, including medical reports and witness testimonials, can streamline this process. Once you’ve made the initial reports, focus on cooperating fully with any insurance investigations or inquiries. Ensuring transparency in communication between all parties can facilitate a smoother resolution.

It’s also beneficial to engage legal counsel specializing in employment law to guide you through the intricacies of the case. This professional can help you understand your rights and navigate the legal system more effectively. Concurrently, review your safety and management processes to identify improvements that can prevent similar incidents in the future. Through careful preparation and agile response, contractors can mitigate the financial and operational impact of employee injury lawsuits, safeguarding their business against long-term repercussions.

Securing Your Business: A Final Word

Being well-informed about insurance for employee injury lawsuits is essential for New York-based contractors. By understanding the different types of coverage and knowing your legal obligations, you can protect your business from financial risks. With the right policies in place, you can focus on growing your business confidently. Visit our homepage for more resources and assistance in securing the best insurance for your needs.

About BGES Group

Running a business is challenging enough without having to spend valuable time dealing with insurance issues. At BGES Group, we make insurance simple by providing responsive, personalized service and helping you secure the right coverage at competitive rates. With more than 45 years of industry experience and access to over 25 top-rated insurance carriers, we take the time to understand your business and design insurance solutions that protect your company, employees, assets, and future—without paying for coverage you don’t need.

Our clients appreciate having one dedicated insurance professional, fast certificate processing, prompt answers, and direct access to a real person when they call. We proactively solve problems before they become costly, help control insurance expenses, and provide expert guidance on Workers’ Compensation, General Liability, Commercial Auto, Umbrella Liability, and other business insurance needs. Our goal is simple: make insurance one less thing for you to worry about while providing the peace of mind that comes from knowing an experienced professional is looking out for your business.

Contact BGES Group Insurance Services

Gary Wallach, President

Licensed in New York, New Jersey & Connecticut

📞 (914) 806-5853

✉️ bgesgroup@gmail.com

🌐 www.bgesgroup.com