Looking for a 100% Reliable Insurance Agency? Your Search May Finally Be Over.

If you’re a New York contractor, you already know how difficult it can be to find a truly reliable insurance broker.

Many contractors have experienced the frustration of calling their insurance agency and getting voicemail. Others wait days for a certificate of insurance. Some receive advice from people who don’t understand construction operations, New York labor laws, contractual risk transfer, workers’ compensation issues, or the unique challenges contractors face every day.

The truth is that not all insurance agencies are created equal.

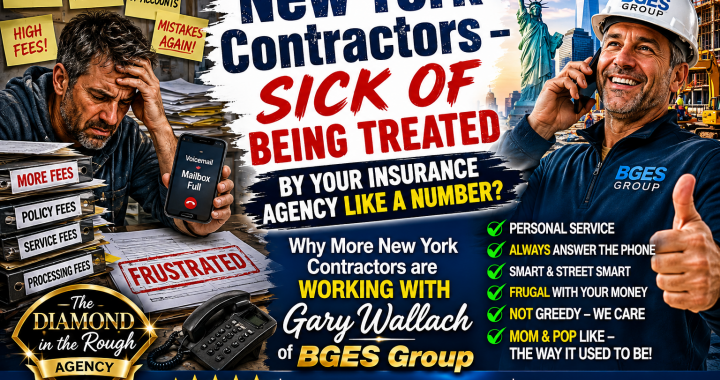

Some agencies operate like factories. One account manager may be responsible for 150 to 200 accounts. Calls go unanswered. Emails sit in inboxes. Certificates take hours or days. Coverage gaps aren’t discovered until there’s a claim.

When you’re running a construction company, that kind of service can cost you contracts, money, and sleepless nights.

That’s why many New York contractors are making the switch to BGES Group.

The Diamond in the Rough

Every once in a blue moon, you find a company that does things differently.

A company that still believes in answering the phone.

A company that believes expertise matters.

A company that understands that contractors need solutions—not excuses.

That’s BGES Group.

We are not a giant corporate agency.

We are not a call center.

We are not a revolving door of account managers.

We are a boutique insurance agency that specializes in helping New York contractors protect their businesses, secure contracts, and grow with confidence.

Our clients know exactly who they are dealing with.

When you call, you speak with someone who knows construction insurance inside and out.

Someone who understands certificates, additional insured requirements, hold harmless agreements, workers’ compensation classifications, umbrella liability, builders risk, commercial auto, and contractor-specific exposures.

Most importantly, someone who genuinely cares about helping your business succeed.

New York Construction Specialists

Construction insurance in New York is not the same as insurance in other states.

The risks are different.

The laws are different.

The claims environment is different.

The coverage requirements are different.

Unfortunately, many agencies treat construction insurance like every other type of business insurance.

That can be a costly mistake.

At BGES Group, New York contractors are our specialty.

For decades, we have focused on helping contractors navigate the complex insurance marketplace.

Whether you’re a:

- General Contractor

- Roofing Contractor

- Restoration Contractor

- Electrical Contractor

- Plumbing Contractor

- HVAC Contractor

- Masonry Contractor

- Excavation Contractor

- Carpentry Contractor

- Painting Contractor

We understand the challenges you face and know where to find the coverage solutions that make sense for your business.

Good Coverage at Competitive Pricing

Most contractors want two things:

- The right coverage.

- A fair price.

Unfortunately, some brokers focus only on price.

Others focus only on coverage.

At BGES Group, we believe contractors deserve both.

Our goal is to find the strongest coverage available while helping you obtain competitive pricing from quality insurance carriers.

We take the time to understand your operation, your goals, and your risk profile.

That allows us to negotiate effectively on your behalf and recommend coverage that protects your company without unnecessary surprises.

Insurance should give you peace of mind—not create more problems.

We Answer the Phone

This shouldn’t be a competitive advantage.

But unfortunately, in today’s world, it often is.

When contractors have an urgent issue, they don’t want to wait three days for a response.

They need answers now.

At BGES Group, responsiveness is part of our culture.

Questions get answered.

Problems get solved.

Urgent issues get addressed.

Clients know they can reach us when they need us.

That’s how business relationships should work.

Certificates Issued in Minutes

Every contractor knows the feeling.

You’re ready to start a job.

The customer needs a certificate.

The property manager needs additional insured wording.

The general contractor needs proof of coverage.

And everyone needs it immediately.

At BGES Group, we understand that certificates are often the lifeblood of your business.

That’s why we pride ourselves on issuing certificates quickly and accurately.

Our goal is simple:

Get you what you need so you can get to work.

Not tomorrow.

Not next week.

Today.

Knowledgeable, Practical, and Tough

A great insurance broker needs more than textbook knowledge.

They need real-world experience.

They need to understand how construction projects actually work.

They need to understand what happens when claims occur.

They need to know how insurance companies think.

They need to know how underwriters evaluate risk.

They need to know how to advocate for their clients.

At BGES Group, we combine decades of industry knowledge with practical, real-world experience.

We’re educated enough to understand complex insurance issues.

We’re experienced enough to solve real problems.

And we’re tough enough to fight for our clients when it matters most.

Contractors don’t need a broker who simply processes paperwork.

They need a broker who becomes part of their team.

From Frustration to Confidence

Many contractors come to us after years of frustration.

They are tired of unanswered calls.

Tired of delays.

Tired of confusion.

Tired of feeling like just another account number.

Then something changes.

They finally have a broker who answers.

A broker who explains things clearly.

A broker who understands construction.

A broker who responds quickly.

A broker who works hard for them.

The result is greater confidence, less stress, and more time to focus on running their business.

That’s the difference the right insurance broker can make.

Why Contractors Choose BGES Group

- New York construction insurance specialists

- Decades of contractor insurance experience

- Personalized service

- Fast response times

- Certificates issued quickly

- Competitive insurance solutions

- Workers’ compensation expertise

- General liability expertise

- Umbrella liability expertise

- Commercial auto expertise

- Builders risk expertise

- Real people answering the phone

- Long-term relationships built on trust

Ready for a Better Insurance Experience?

If you’re tired of dealing with agencies that don’t return calls, don’t understand construction, and don’t provide the level of service your business deserves, maybe it’s time for a change.

The right insurance broker doesn’t just sell insurance.

The right broker protects your company, solves problems, saves time, and helps you win more business.

At BGES Group, that’s exactly what we strive to do every day.

Contact BGES Group

BGES Group

New York Construction Insurance Specialists

Serving Contractors Throughout New York, New Jersey, and Connecticut

Phone: (914) 806 5853

Contact: Gary Wallach

E-mail: bgesgroup@gmail.com

Website: www.bgesgroup.com

If you’re looking for an insurance agency that is reliable, knowledgeable, responsive, and committed to helping your business succeed, contact BGES Group today and discover why many contractors consider us the diamond in the rough they’ve been searching for.