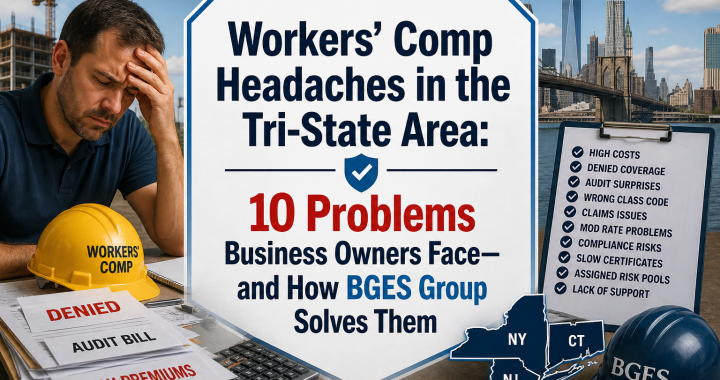

Workers’ compensation insurance is one of the most important protections a business can have. It safeguards your employees after workplace injuries while also protecting your company from potentially devastating financial exposure. But finding the right workers’ compensation policy is not always easy. Rising premiums, confusing audits, classification code issues, payroll reporting requirements, claims concerns, and changing carrier appetites can make the process stressful and time-consuming.

If you are searching for a new workers’ compensation policy, the key is not just finding coverage — it is finding the right partner to help you manage the policy before, during, and after the sale.

That is where BGES Group comes in.

At BGES Group, we understand that business owners need more than an insurance policy. They need guidance, responsiveness, problem-solving, and someone who understands how workers’ compensation really works in the real world.

Why Businesses Shop for a New Workers’ Compensation Policy

Many companies begin looking for a new policy when they experience one or more of the following issues:

- Large premium increases

- Poor claims handling

- Non-renewal notices

- Payroll audit disputes

- Difficulty obtaining certificates

- Incorrect classification codes

- Lack of communication from their current agent

- Problems with subcontractor compliance

- Coverage gaps

- Trouble obtaining required endorsements

The truth is that workers’ compensation insurance is not “one size fits all.” Every business has different operations, payroll structures, subcontractor exposures, and state requirements. Having an experienced insurance professional can make a major difference in cost, compliance, and overall experience.

10 Ways BGES Group Makes Your Workers’ Compensation Policy Easier to Manage

1. We Help You Find Competitive Coverage Options

BGES Group works with multiple insurance carriers and markets to help find coverage solutions that fit your business operations and budget. Whether you are a small contractor, staffing company, manufacturer, transportation company, or office operation, we work to locate appropriate options for your industry.

2. We Help Correct Classification Issues

Incorrect class codes can dramatically increase your premiums. We review operations carefully to help identify potential classification problems that may be costing your business unnecessary money.

3. We Assist With Audit Preparation

Workers’ compensation audits can be stressful and expensive if records are not organized properly. We help clients prepare payroll records, subcontractor certificates, and documentation ahead of time to help avoid surprises.

4. We Help With Certificates of Insurance

Many businesses need certificates issued quickly for contracts, landlords, vendors, and project owners. BGES Group helps streamline the certificate process so you can focus on running your business.

5. We Help Manage Subcontractor Compliance

If you use subcontractors, missing certificates or improper documentation can create major audit issues. We help clients understand what documentation is needed and how to maintain proper records.

6. We Explain Coverage in Plain English

Insurance policies can be confusing. We take the time to explain your policy, endorsements, exclusions, audits, and obligations in a straightforward manner so you understand what you are purchasing.

7. We Help Businesses With Difficult Situations

Some companies struggle to obtain coverage because of claims history, lapse in coverage, high-risk operations, or rapid growth. BGES Group works with businesses facing challenging insurance situations and helps explore available solutions.

8. We Provide Ongoing Service Throughout the Policy Term

Many agencies disappear after the policy is issued. At BGES Group, we continue helping clients throughout the year with policy changes, payroll adjustments, certificates, claims questions, and audit concerns.

9. We Help Control Long-Term Insurance Costs

Workers’ compensation premiums are affected by payroll, claims history, experience modification factors, and operational changes. We help clients understand how these factors impact premiums and discuss strategies that may help improve future insurance costs.

10. We Value Relationships and Responsiveness

When business owners have questions or urgent issues, they need answers quickly. BGES Group believes communication matters. We work hard to provide responsive service and practical solutions when clients need assistance.

Why Choosing the Right Insurance Partner Matters

A workers’ compensation policy is not just another bill. It is an important part of protecting your employees, your contracts, and your business operations.

The wrong policy structure or lack of guidance can create expensive problems, including:

- Large audit balances

- Coverage disputes

- Contract compliance issues

- Claims complications

- Penalties from state agencies

- Difficulty obtaining future coverage

Having an experienced insurance professional on your side can help reduce confusion and make the process smoother from start to finish.

About BGES Group

BGES Group is committed to helping businesses navigate the complex world of commercial insurance. We work with companies in a variety of industries and understand the unique challenges business owners face every day.

Our goal is to provide practical insurance solutions combined with responsive personal service. We believe clients deserve honest communication, attention to detail, and a professional who advocates for their business.

Whether your company is searching for a new workers’ compensation policy, reviewing current coverage, handling an audit issue, or trying to improve insurance costs, BGES Group is here to help.

We understand that every business is different. That is why we take the time to learn about your operations, workforce, contracts, and goals before recommending insurance solutions.

How BGES Group Can Help Your Business

BGES Group assists businesses with:

- Workers’ compensation insurance

- General liability insurance

- Excess liability coverage

- Commercial auto insurance

- Certificates of insurance

- Additional insured requirements

- Waiver of subrogation requests

- Audit preparation assistance

- Contractor insurance compliance

- Risk management guidance

Our mission is simple: help business owners protect what they have built while making the insurance process easier and more manageable.

Contact BGES Group Today

If you are looking for a new workers’ compensation policy or simply want a second opinion on your current coverage, BGES Group is ready to help.

Contact:

Gary Wallach

BGES Group

Phone: 914-806-5853

Email: bgesgroup@gmail.com

Website: www.bgesgroup.com

The right workers’ compensation policy can protect your employees, support your business operations, and help you avoid costly problems down the road. Let BGES Group help make the process easier, clearer,